Bigger Isn’t Delivering Better Returns

Why India’s hotel developers may be overbuilding guestrooms.

By Suman Tarafdar

For decades, Indian hotel development has been guided by an almost reflexive belief: larger rooms signal higher quality, command higher rates, and ultimately deliver better returns. The logic feels intuitive. More space suggests greater comfort, stronger positioning, and a competitive edge in a market where aspiration often shapes product decisions.

Yet the data tells a different story. According to Hotelivate’s analysis of branded hotel performance across India for 2024–25, the relationship between room size and RevPAR is far weaker than most developers assume (Does Size Really Matter by Megha Tuli and Mihir Chalishazar) in many cases, larger rooms not only fail to generate higher revenue but can actively erode project economics by reducing key count, increasing capital expenditure, and diluting return on investment.

At an average development cost of approximately ₹11,300 per sq.ft., incremental space is expensive space. When additional square metres fail to translate into proportionate revenue gains, they represent locked-in inefficiency—a structural decision that cannot easily be reversed once construction is complete.

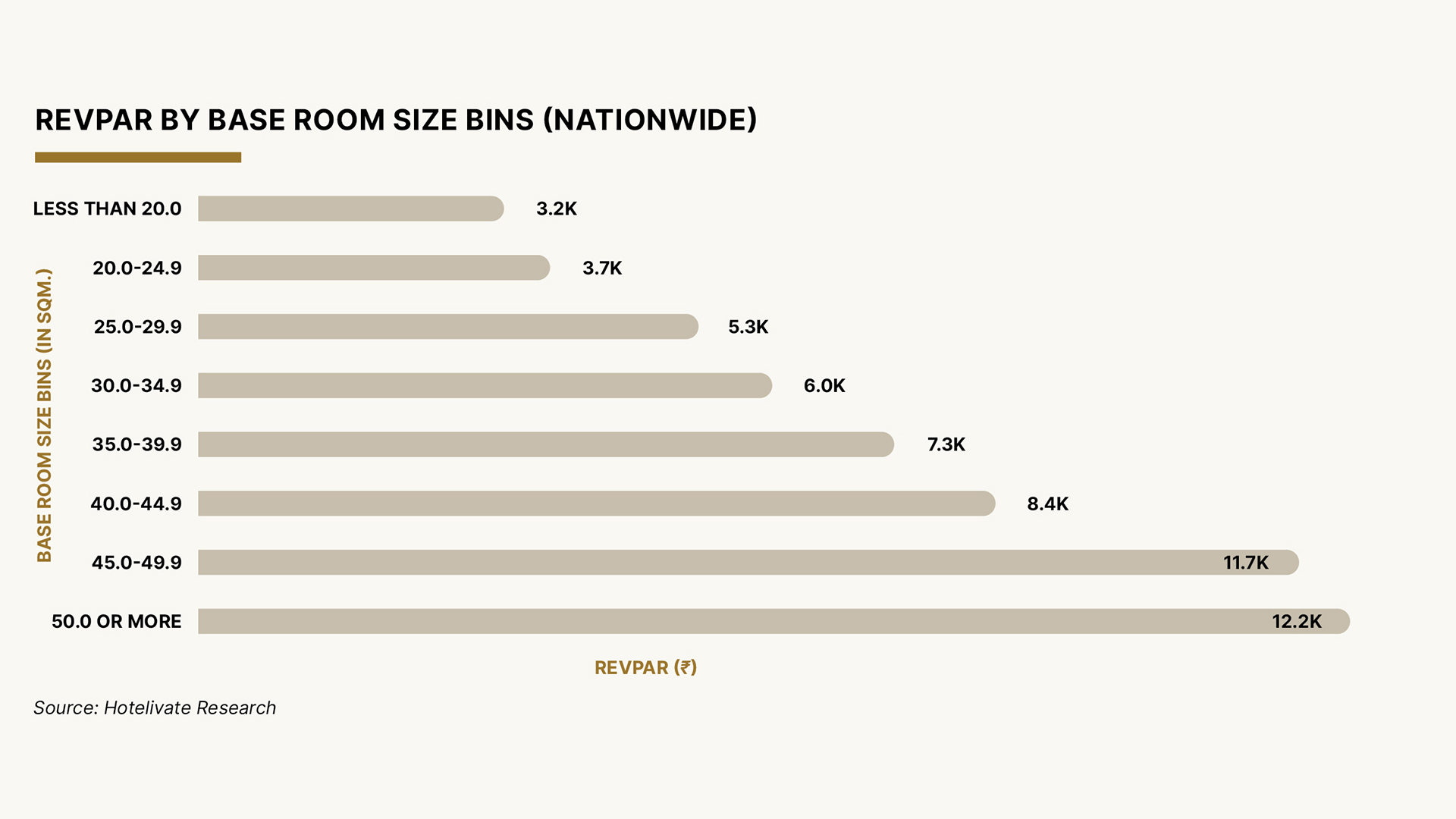

When bigger stops delivering better

Hotelivate analysed the correlation between base room size and RevPAR across branded hotels in India, segmenting the dataset by location type, administrative zone, brand origin, hotel inventory size, city tier, and positioning. Across segments, the conclusion remains consistent: beyond a certain threshold, larger guestrooms produce diminishing financial returns.

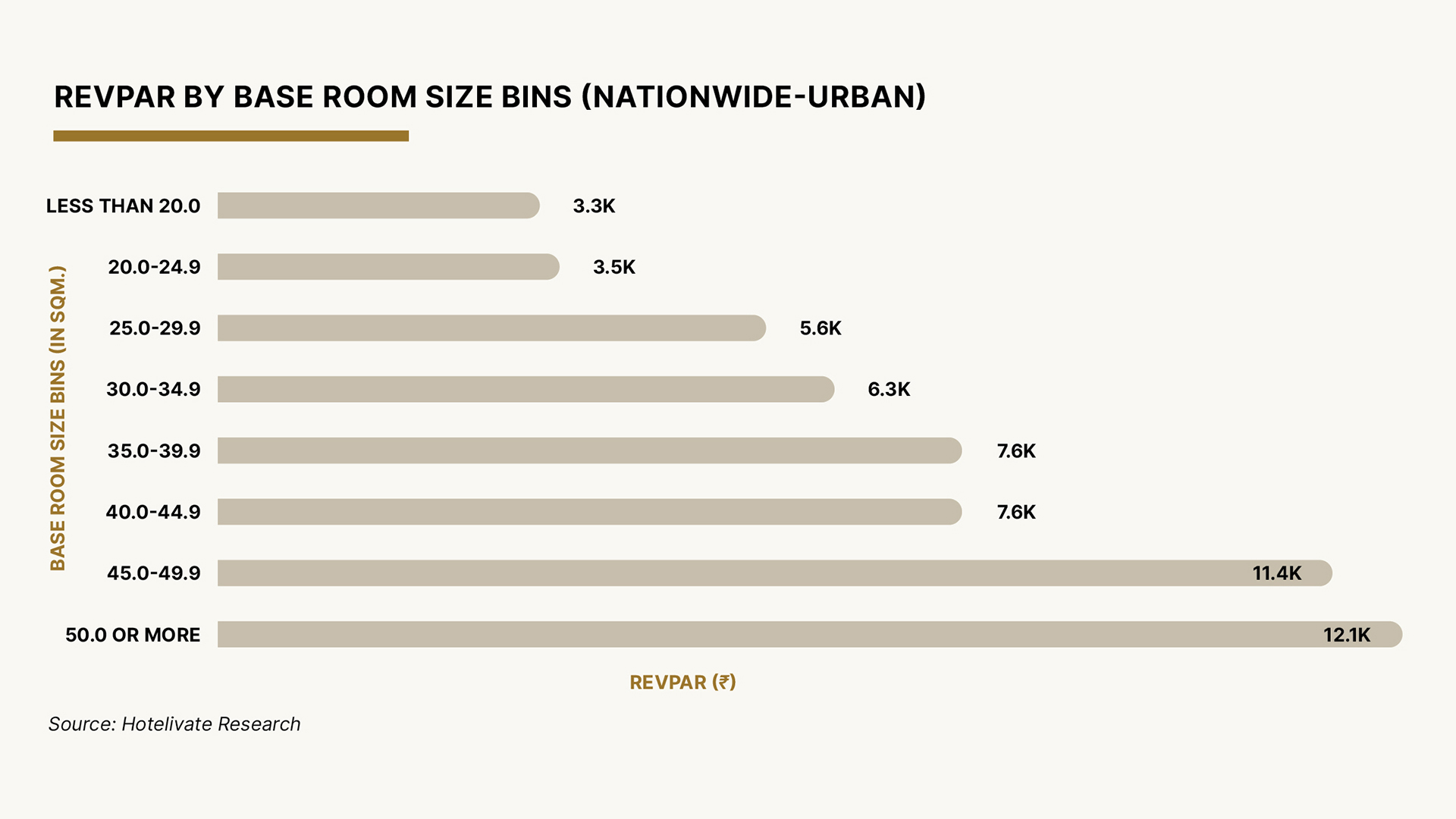

Urban hotels: a 30% size difference with no RevPAR upside

Urban hotels represent approximately 55% of Hotelivate’s dataset. Within this segment, properties with base room sizes between 35sqm. and 45sqm. achieve broadly similar RevPAR performance.

In practical terms, this means that increasing room size by approximately 30% does not yield a significant improvement in revenue performance. Developers who expand room footprints by an additional 10sqm. incur significant construction cost increases without a corresponding uplift in yield.

The implication is clear: incremental space does not automatically translate into incremental value.

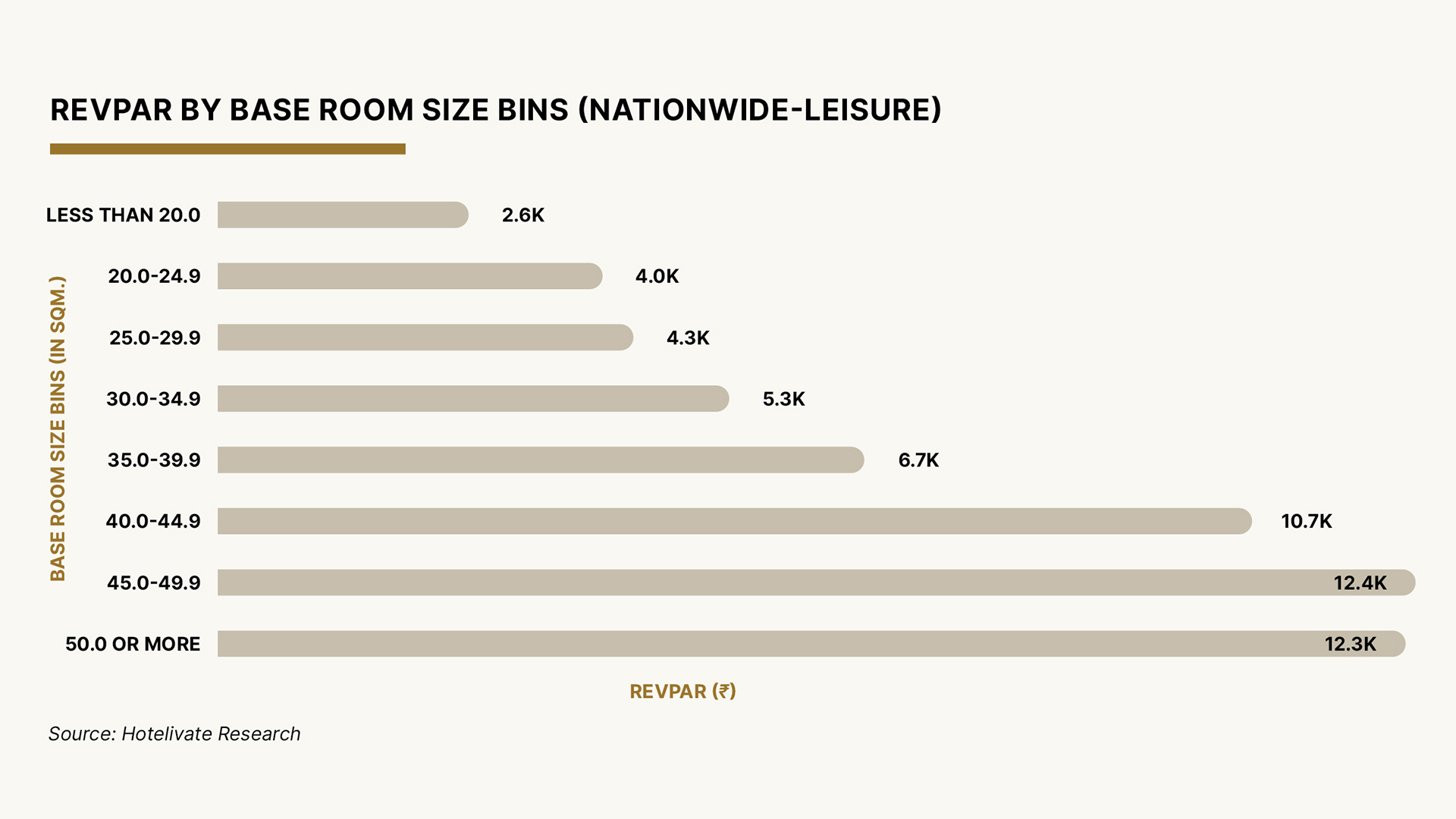

Leisure hotels: when more space can reduce performance

The leisure segment, representing roughly 45% of the sample, produces one of the most striking insights in the analysis. Hotels with base room sizes between 45sqm. and 50sqm. outperform those with rooms exceeding 50sqm.

Increasing room size by at least 11% beyond this range does not merely plateau performance—it correlates with lower RevPAR. This finding reinforces an important structural reality of leisure demand: the destination itself is the primary driver of guest choice.

Landscape, experiences, amenities, and atmosphere shape pricing power far more than marginal increases in room size. As Hotelivate notes, allocating additional floor area to guestrooms in leisure destinations often diverts capital away from public spaces, amenities, and experiential elements that influence guest satisfaction more directly.

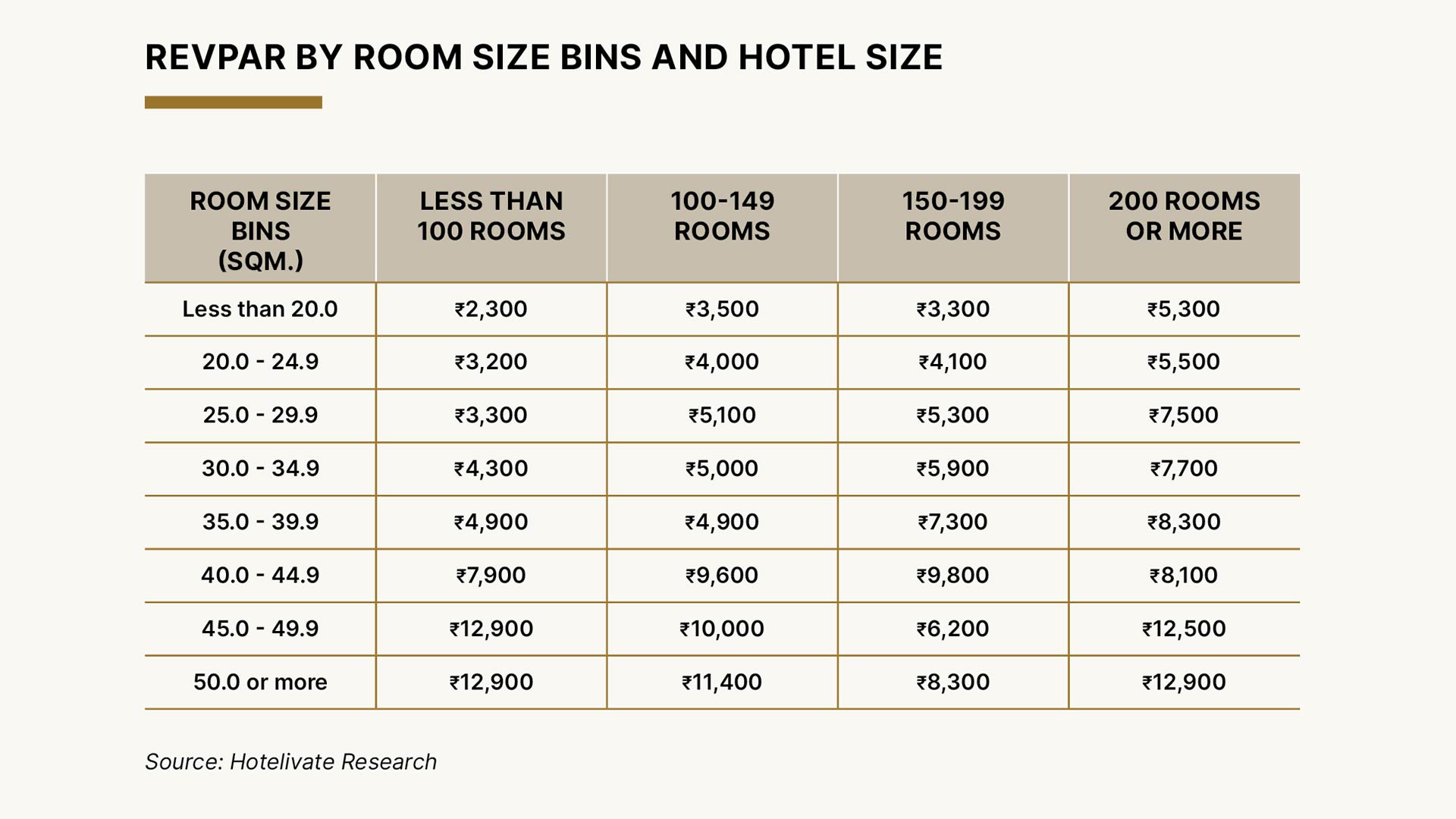

Hotel size lens: more space, fewer returns

Inventory size further highlights the economic trade-offs of oversized guestrooms.

Among hotels with 100–149 keys (approximately 17% of the sample), RevPAR remains consistent across room sizes ranging from 25sqm. to 40sqm.—a 60% variation in spatial allocation. At the upper end of this range, RevPAR performance declines. Similarly, for hotels with 150 keys or more (approximately 18% of the sample), the 25–35sqm. range delivers stable performance with no discernible benefit from increasing room size by up to 40%.

Larger rooms reduce the number of keys that can be accommodated within a given built-up area. Fewer keys translate into lower revenue potential per sq.ft. of development, directly impacting project IRR.

Tier 2 and Tier 3 markets: where overbuilding risks are highest

In Tier 2 and Tier 3 cities, the performance gap becomes even more pronounced. Hotels with base room sizes between 45sqm. and 50sqm. perform at par with, or better than, properties offering rooms above 50sqm.

In these markets, demand is often more price-sensitive and less dependent on spatial luxury. Overspecifying guestrooms increases capital intensity without improving revenue outcomes, placing pressure on project viability.

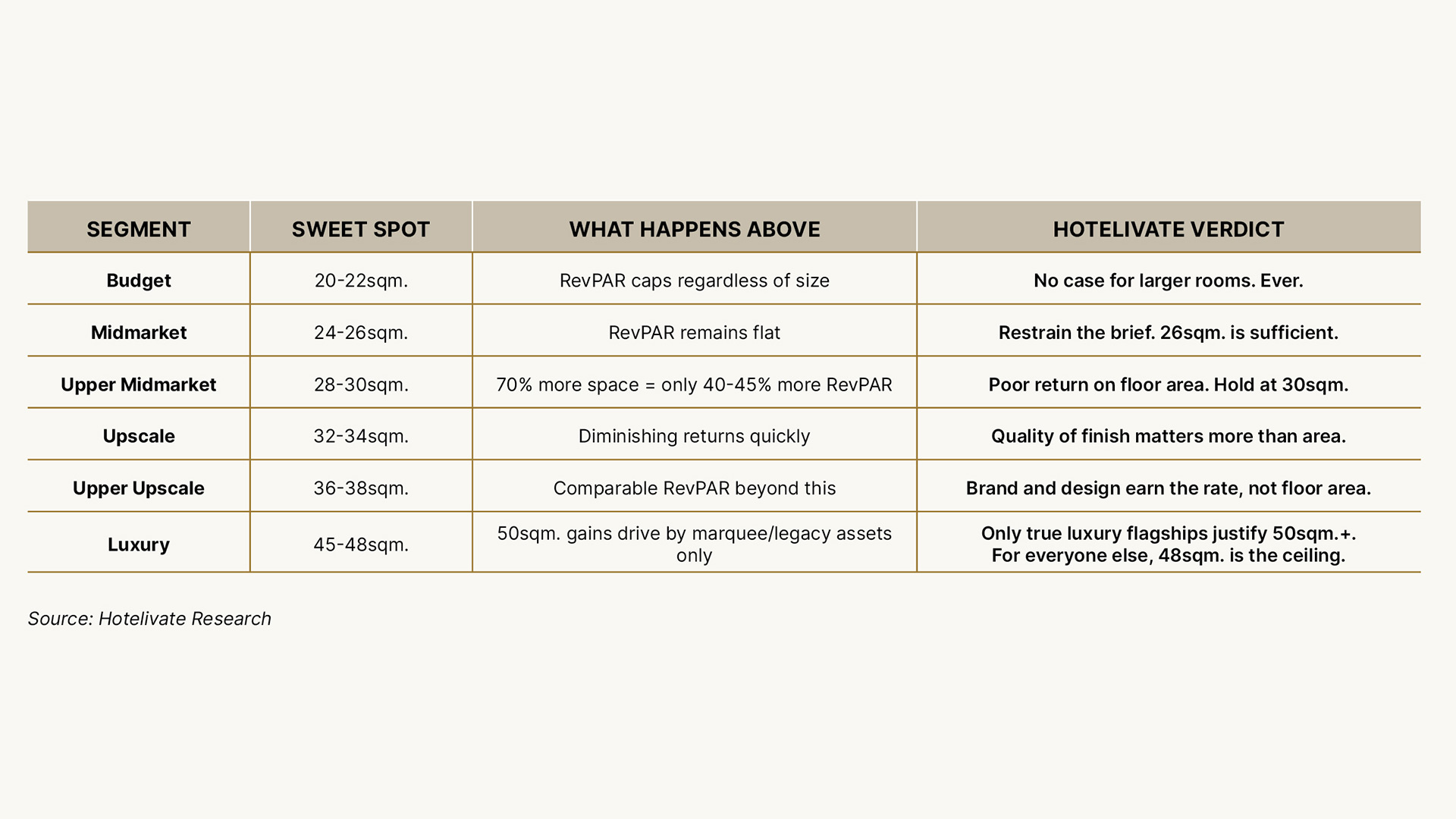

Identifying the “sweet spot” in room sizing

One of the most actionable insights from Hotelivate’s research is the identification of an optimal room size band where RevPAR performance stabilises relative to development cost.

Across multiple segments, guestrooms between 35sqm. and 50sqm. demonstrate comparable performance outcomes. Beyond this range, additional square footage generates limited—and sometimes negative—revenue advantage. This plateau suggests that developers should treat room size as an optimisation exercise rather than a branding statement.

Once rooms exceed approximately 50sqm., the marginal return on each additional square metre declines sharply.

India’s rooms are already generous by global standards

Indian hotel rooms are, in many cases, already larger than global benchmarks.

According to The Leela Industry Report (2025), the average luxury hotel room size in India is approximately 45sqm. Global benchmarks from SiteMinder and Ming Sun Design Standards indicate that efficient urban hotels internationally often operate with significantly smaller room footprints:

- Typical global standard rooms: 20–30sqm.

- Upper upscale rooms: 30–40sqm.

- Suites: 50–80sqm.

Compared to these benchmarks, India’s spatial standards are relatively generous, particularly in urban markets where land and construction costs continue to rise.

Pipeline growth makes efficiency more urgent

Design discipline becomes increasingly important as India’s hotel supply pipeline expands. Horwath HTL estimates that India’s branded hotel inventory will reach approximately 105,000 additional rooms by 2029, representing substantial growth relative to the current supply base. If oversized guestrooms continue to be replicated across this pipeline, inefficiencies will be embedded at scale. Also, strong operating performance may temporarily mask cost implications of spatial over-specification.

According to HVS ANAROCK’s 2024 industry overview:

- National occupancy levels remain strong at 63–65%.

- Average Room Rates (ARR) are approximately ₹7,800–₹8,000.

- RevPAR has grown 27–29% compared to pre-pandemic benchmarks.

Favourable trading conditions can absorb higher capital costs in the short term. However, structural inefficiencies become more visible as market cycles normalise.

The structural constraint

Room size decisions also influence the total number of keys a hotel can accommodate within a given development envelope.

Data from the Ministry of Tourism’s Indian Hotel Industry Survey indicates:

- Average hotel size historically: 76 rooms

- Average five-star hotel: 148 rooms

- Average five-star deluxe hotel: 225 rooms

Increasing room size reduces the number of keys achievable on a site, lowering potential revenue per sq.ft. and weakening yield efficiency. Because hotels are long-term assets, design decisions made during planning shape financial performance for decades. Unlike pricing or operational strategies, room size cannot easily be adjusted once the building is complete.

What actually drives hotel performance

Hotelivate’s analysis reinforces a broader industry truth: room size is not a primary driver of RevPAR performance. Instead, performance is more closely linked to:

- Location: A well-located hotel consistently outperforms a poorly located one, regardless of room dimensions.

- Brand strength and distribution reach: Brands with strong reservation networks and loyalty ecosystems deliver occupancy advantages that outweigh incremental increases in room size.

- Product-market fit: Hotels designed around the needs of their specific demand segments—rather than generic design assumptions—demonstrate stronger commercial outcomes.

- Experience design: Public spaces, food and beverage programming, wellness facilities, and destination-driven experiences often have a greater influence on guest satisfaction and pricing power than marginal increases in room area.

- Longevity and character: As holding periods extend, brand equity, design relevance, and narrative identity differentiate top-performing assets.

Build smarter, not bigger

India’s hotel development cycle is entering a period of accelerated expansion, with more than 120,000 rooms currently in the pipeline, representing over half of the existing supply base. The opportunity is significant. But so is the risk of embedding inefficient design decisions that compromise long-term returns.

Hotelivate’s analysis provides a clear takeaway: once guestrooms reach the optimal size range, additional square footage adds cost without adding value. In an environment where land, construction, and capital costs continue to rise, disciplined design decisions are no longer optional; they are essential.

The next generation of high-performing hotel assets is unlikely to be defined by the largest rooms, but by the most carefully calibrated ones. Right-size the room. Right-size the return.