India Hospitality Market Records USD 567 Million Investments in 2025, Up 67% YoY: JLL Report

India’s hospitality sector witnessed a strong resurgence in investment activity during 2025, driven by improving operating performance, rising domestic travel demand, and growing investor confidence in the long-term fundamentals of the market.

Hotel investments during the year reached approximately USD 567 million across 28 transactions, representing a significant increase over 2024 levels. Momentum has continued into Q1 2026, with transaction activity remaining robust amid sustained interest from institutional investors, listed hotel companies, private equity firms, family offices, and high-net-worth individuals.

By SOH Edit Team

Expansion Beyond Metro Markets

The market continues to evolve beyond traditional gateway cities, with Tier II and III destinations emerging as key growth centers for hospitality investments and branded hotel development.

Nearly 40% of overall transaction activity during the year originated from emerging cities and leisure destinations such as Rishikesh, Goa, Ludhiana, Nashik, Vadodara, Udaipur, and Lonavala, reflecting increasing investor confidence in the long-term demand potential of these markets. This trend has also been reinforced by the rapid expansion of organized hospitality supply, with branded hotel signings reaching over 51,000 keys across 424 hotels during the year, marking a substantial increase compared to the previous period. A significant majority of these signings were concentrated in Tier II and III cities, highlighting the continued penetration of organized hospitality into underserved markets.

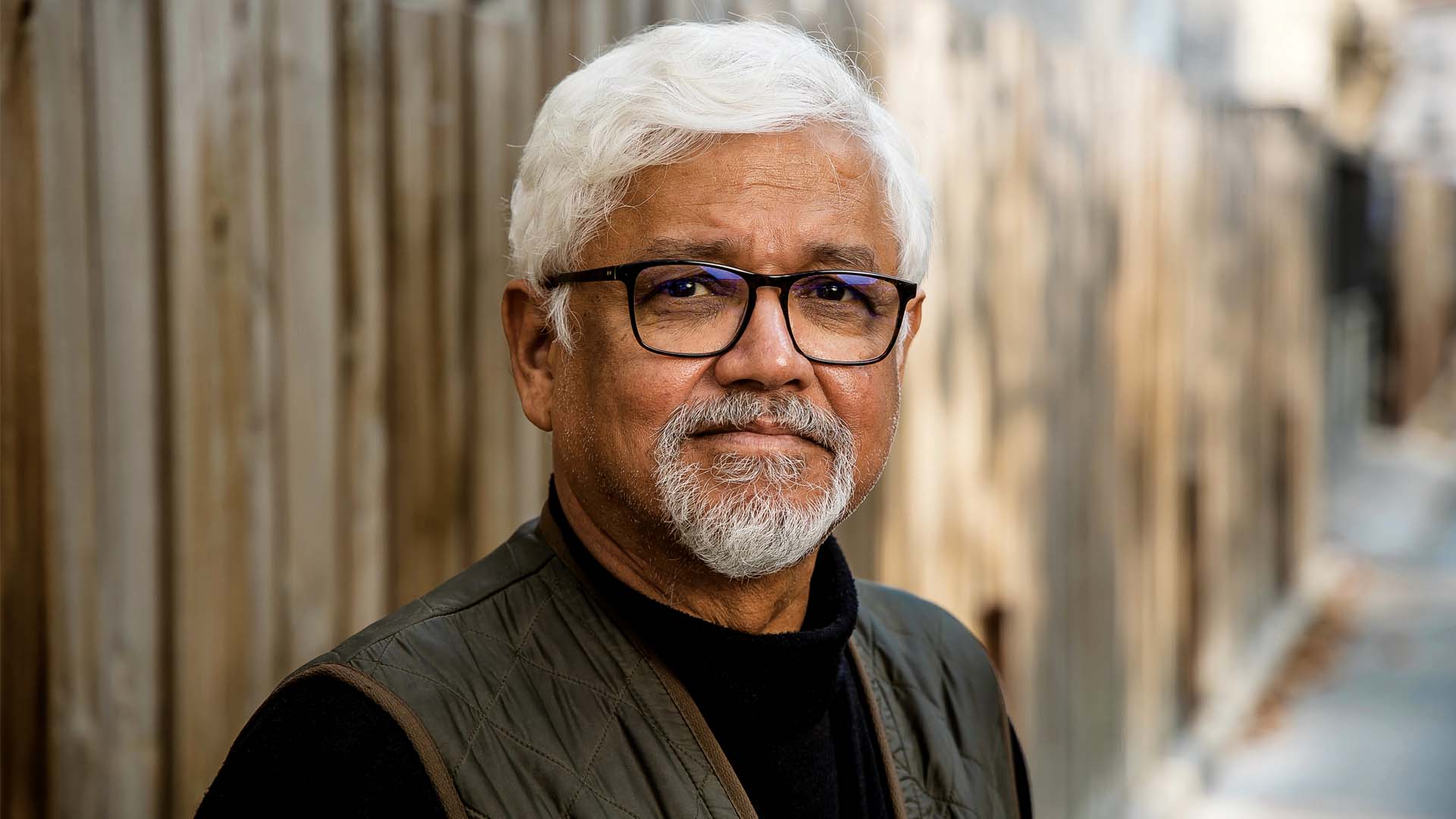

Gaurav Sharma, Managing Director, Hotels, India & Senior Director, Hotels Capital Markets, Asia,JLL said, “India’s hotel investment market is reflecting a clear step-up in both investor confidence and market depth, with rising transaction activity supported by a broader mix of institutional and domestic capital. What is particularly encouraging is the continued expansion beyond gateway cities, with Tier II and III markets steadily evolving into more mature, investment-grade destinations backed by improving operating performance and scalability. The momentum has carried strongly into 2026, with a robust start to the year underscoring sustained capital appetite.”

Investor preference remained heavily skewed toward operational and income-generating assets, which accounted for the majority of transaction activity during the year. Luxury and upscale hotels continued to dominate investment interest as investors focused on high-quality assets capable of delivering stable cash flows and long-term value appreciation. The premium hospitality segment has particularly benefited from strong domestic leisure travel, improving corporate demand, and increasing international inbound traffic, resulting in sustained occupancy growth and rate expansion across key markets.

Gaurav Sharma, Managing Director, Hotels, India & Senior Director, Hotels Capital Markets, Asia,JLL.

Development & Brand Expansion

Development activity also remained strong throughout the year, with greenfield projects accounting for a substantial share of the upcoming hospitality pipeline. Large-format hotels with over 250 keys witnessed increased traction, supported by rising demand in both metropolitan and emerging business destinations. While Tier I cities continued to account for a major portion of new development activity, several emerging markets including Guwahati, Visakhapatnam, Indore, and Pushkar also witnessed significant expansion momentum. The industry’s continued shift toward asset-light operating structures was further evident in the increasing share of management contract-based signings, reflecting operators’ preference for scalable and capital-efficient growth models.

Institutional participation within the hospitality sector has also become increasingly sophisticated, with investors pursuing platform-level acquisitions, strategic partnerships, and portfolio consolidation opportunities. Capital deployment toward such strategic investments remained strong during the year, highlighting growing confidence in India’s long-term hospitality growth story. The sector continues to benefit from broader structural tailwinds including infrastructure expansion, airport-led development, improved regional connectivity, government-led tourism initiatives, and urban development programs across key growth corridors such as Yashobhoomi in Delhi, Neopolis in Hyderabad, Fintech City in Chennai, and the Jewar Airport region.

Market Outlook for 2026

Looking ahead, the outlook for India’s hospitality investment market remains positive, supported by strong domestic travel demand, expanding infrastructure, increasing institutional participation, and continued supply growth in emerging markets. Limited availability of high-quality operational assets is expected to sustain investor competition and support asset valuations across premium hospitality segments. While geopolitical uncertainties and capital market volatility may pose near-term challenges, India’s resilient domestic tourism base and evolving hospitality ecosystem are expected to provide long-term stability and growth opportunities for investors and operators alike.

Overall, the Indian hospitality sector continues to strengthen its position as one of the most attractive investment destinations within the Asia-Pacific region, supported by rising capital inflows, expansion into emerging markets, growing organized supply, and sustained demand across premium hospitality segments.