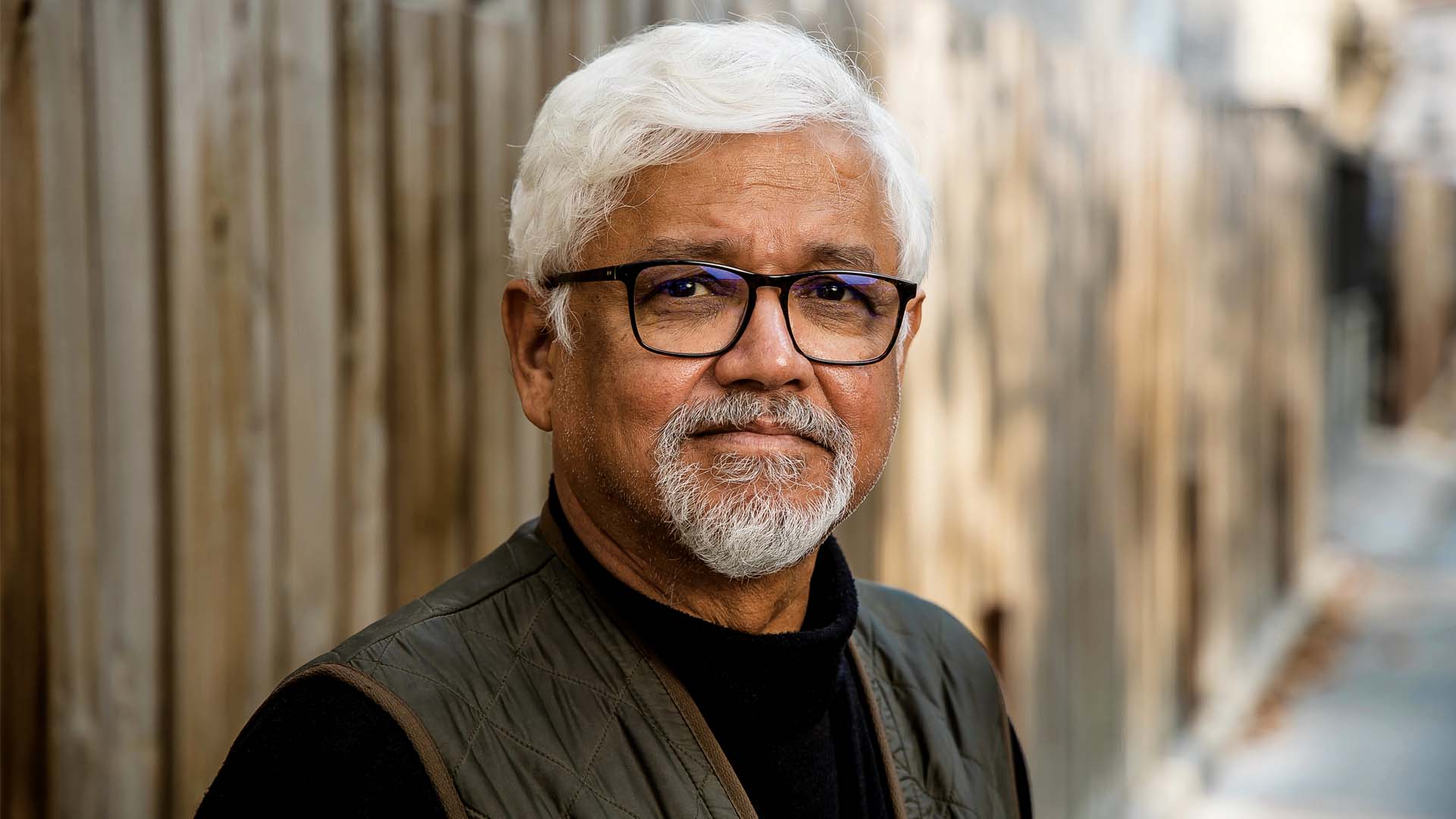

Legacy, In Acceleration

Decisive. Relentless. All in. IHCL's MD & CEO Puneet Chhatwal on translating ambition into sustained growth.

By Deepali Nandwani

The gregarious, innovation-driven MD & CEO of IHCL, Puneet Chhatwal, is fond of saying that strategy talks but execution walks—a line that sounds aphoristic until one realises it is also a précis of his own career. In a sector often drawn to nostalgia and inherited grandeur, Chhatwal has shaped a leadership vocabulary anchored in resilience and compassion, tempered by commercial discipline. He treats culture not as an ornament but as an operating system. A self-described product of the East and the West, he combines the reflexes of a global hotelier with the instincts of an Indian institution-builder.

When he assumed leadership of Indian Hotels Company Limited (IHCL), the Tata Group’s century-old hospitality arm, its market capitalisation stood at just under ₹13,000 crore. Under his tenure, it has crossed ₹1 lakh crore, an expansion that reflects not only financial rigour but careful narrative repositioning. Chhatwal has guided IHCL beyond the nostalgia for legacy assets towards a portfolio that balances heritage with momentum and a data-literate culture that still insists hospitality remains, at heart, a human act.

His leadership style is evangelical about learning: encouraging Ivy League programmes, cross-border exposure, and the belief that experience is the only durable competitive advantage. If relationship capital is hospitality’s true currency, Chhatwal has compounded it by building bridges across geographies, generations, and sensibilities, while demonstrating that scale, in the right hands, need not dilute soul.

Chhatwal has guided IHCL beyond the nostalgia for legacy assets towards a portfolio that balances heritage with momentum and a data-literate culture that still insists hospitality remains a human act.

Indian Hospitality’s Structural Shifts

You’ve led a 120-year-old hospitality institution through enormous change and a lot of crises. When you consider the current state of the industry, do you believe we are entering a transformative phase for hospitality?

The hospitality sector today is definitely in a very different orbit than it was five, seven, or 10 years ago, or 20 or 30 years ago, the reason being that India has changed. The last 10 years have been transformative for India, its economy, and consumer behaviour. Given that it is a large domestic market of 1.5 billion people, everything else has to change with it, and hospitality is no exception. I believe hospitality has evolved beyond being purely customer-service driven. While service remains its core, the definition of what constitutes meaningful service has expanded to include many new dimensions. Some of those include creating shareholder value for all stakeholders—for employees, suppliers, partners, anybody who works in the hospitality ecosystem.

You cannot become the world’s fourth-largest economy, aspiring to become the third-largest, and have the same behaviour pattern as you did at number 20 or 25 or 30. I think it is a continuous evolution process. The change in GDP growth, in the per capita income, and in disposable income is going to drive consumer sectors. And the consumer sectors include travel, tourism, hospitality, and aviation.

Given that India’s hospitality industry remains largely fragmented and unorganised, does the sector need to become more structured? And how can independent hotel groups still organise themselves around certain standards?

What is special about India is its unity in diversity. Whether small, medium, or large, everybody can find space in India. Also, the various states of India are not in the same economic zone. For example, Maharashtra, as the commercial state of India, with Mumbai as its capital, does not equate in the same correlation to many other states of India. When it comes to tourism, there are states such as Goa, UP, because of the Mahakumbh, or Kashmir, which thrive on tourism. But that is not true for many other states in India.

India is what it is, and I don’t think there will be a one-dimensional approach in any sector, including hospitality. There is enough space for small, medium, and large enterprises. Having said that, there is always one or two players that emerge as leaders or the largest in the sector, and we are very privileged to be one of those. And in our 100-plus-year legacy, we continue to drive the values of hospitality as leaders and as those who put hospitality on the map of India.

Despite strong travel demand, supply growth in India’s top 10 destinations has not kept pace. Is this shortage of adequate supply the reason ARR remains elevated, particularly when compared with neighbouring countries?

There is a demand-supply gap as we speak today, but it has not been historically that way. The nature of demand and supply is such that if demand increases and supply lags behind, eventually it catches up. So I do not think that is such a serious issue. India is a large country that is benefiting from immense expenditure on infrastructure, whether in Goa, Rajasthan, or any other part of India. I always call it the renaissance of train stations, millions of square kilometres of highways getting built, doubling of airports…all that is happening.

As a large economy, India’s cost of living is higher than in many other countries, which raises the cost of service and, in turn, the ability—and need—to charge higher rates. That will inevitably place prices above destinations such as Vietnam or Cambodia. But travellers do not come to Goa simply because it is inexpensive. They come for its multicultural character, its Portuguese history, and the way the state transforms into a beautiful place at Christmas. Destinations in India offer many such distinct facets that make them unique and special. It is difficult to compare them with much smaller countries, some of which are smaller than the size of our smallest state.

Do you think the apprehension that more Indians are travelling abroad instead of holidaying in their own country is valid?

Travel should not be construed as domestic only. Just as we want our share of foreign tourist arrivals, other countries also want to attract international tourists. We just need to find a balance in how many are coming in and how many are going out. The likelihood is that the number of people travelling out of India will always be higher than those coming in is because India represents such a large share of the world’s population. It is not an apples-to-apples comparison. The reality is that as Indians acquire the ability to spend money, they do not want to spend all of it in India. When you earn well, you do not put it all into real estate or gold. You may put some into the capital markets and other instruments.

It is good that Indians gain awareness of how things work outside India. It is also good that they travel within India, so they understand how things work in the north of India, in Kanyakumari, Guwahati, or Jamnagar. Cultural understanding improves when there is exposure to different cultures.

You have often spoken about how conferences could shape the future of travel in India. With the government investing in large-scale convention infrastructure, are we attracting events at the scale these venues were designed for, or is this still an early stage?

It’s a very good start. Those facilities are world-class, whether it is Bharat Mandapam (former Pragati Maidan) or Yashobhoomi (Dwarka), including centres built in Goa or in Mumbai with Jio. I think they have captured a latent demand, while also creating infrastructure that enables large organisations to host events in India. That is critical and has helped drive the growth of business events, especially in Delhi and Mumbai.

Do you see hospitality players continuing to develop venues specifically geared towards conferences?

I see at least 10 to 20 convention centres attached to hotels coming up over the next 10 years, at the maximum. Be it Goa or Guwahati, Delhi or Mumbai and Kochi—I think this is going to happen across India. We had a lot to catch up on, and we have got a good start with Mumbai and Delhi; the rest is following rapidly.

From your vantage point, beyond meeting demand, how do you see the hospitality sector evolving as traveller expectations continue to change?

I see hospitality and tourism contributing at least 10% to India’s GDP and over 10% of jobs. This is not a far-fetched number. Rajasthan already contributes around 17%, and Goa is also north of 17% in terms of GDP contribution. There are many destinations in India that have not yet reached their potential.

So, I think much of this will unfold over the next 20–25 years, and you can expect the hospitality sector to play a very important role in job creation, in skilling the nation, and in terms of financial contribution. The thing that has intrigued me post-COVID is that services in the Western hemisphere, from where we learned the business of hospitality, have declined because of an ageing population and rising cost structures. I see this as a significant opportunity for Asian hotel brands in general, and Indian luxury brands in particular, to travel with Indian customers outside India, to destinations they prefer, build hotels there, take Indian hospitality to the world, and make it a global benchmark.

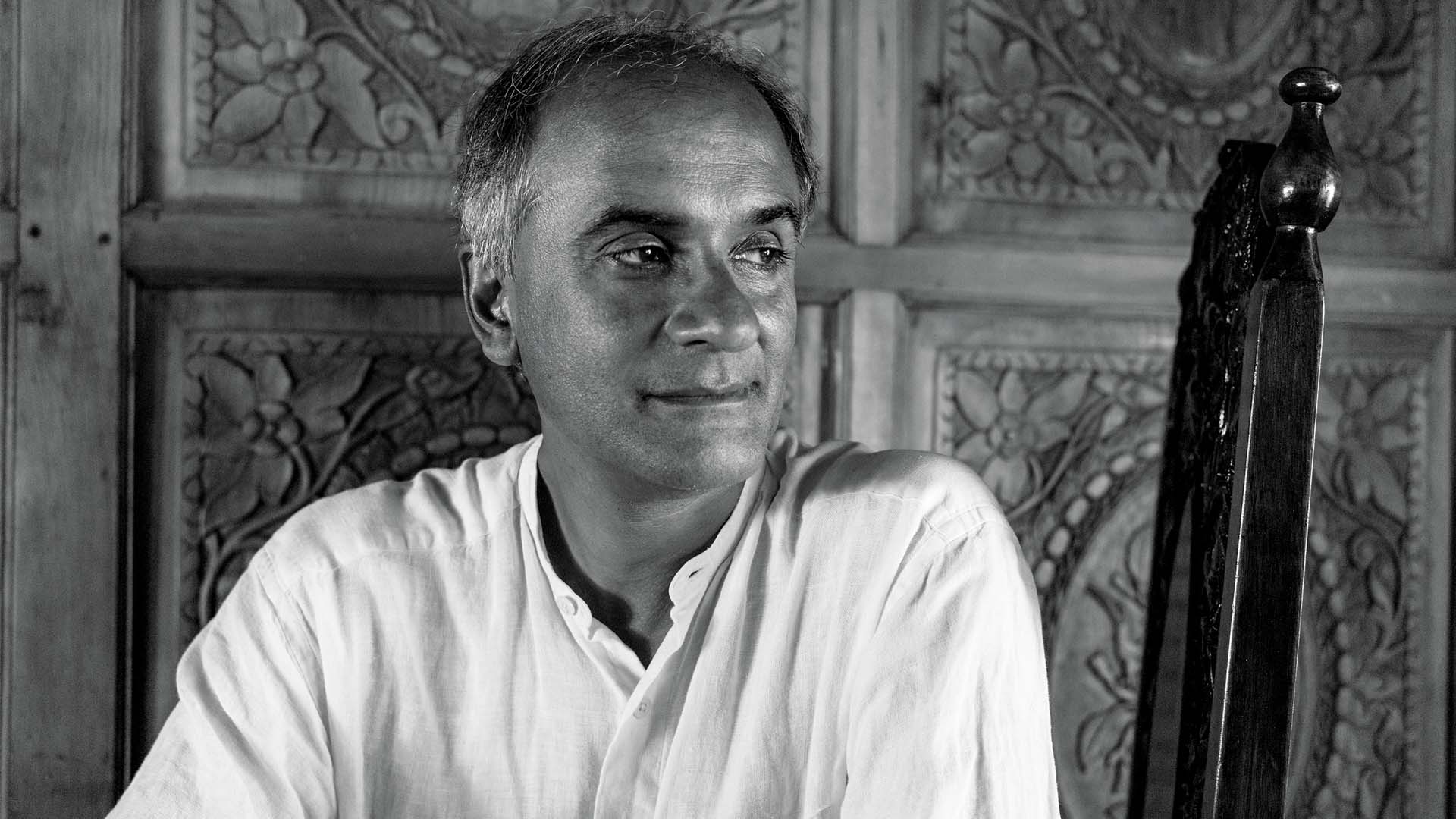

Hospitality has evolved beyond being purely customer-service driven, says Chhatwal.

The thing that has intrigued me post-COVID is that services in the Western hemisphere, from where we learned the business of hospitality, have declined because of an ageing population and rising cost structures. I see this as a significant opportunity for Asian hotel brands in general, and Indian luxury brands in particular, to travel with Indian customers outside India, to destinations they prefer, build hotels there, take Indian hospitality to the world, and make it a global benchmark.

Puneet Chhatwal

MD & CEO, IHCL

That’s a very interesting thought, taking Indian hospitality and Indian hotel brands outside India. Do you see them also attracting international travellers in some way?

For any investment to make sense, you need a certain base business. If you can get it through your own travellers, why not leverage that? For decades, we have dreamt of Switzerland and seen it through the eyes of Bollywood. So why not have the first Indian-branded hotel in Switzerland, in one of those key destinations. I am sure you will get a base occupancy of 30, 40, 50% just from travellers from your home market. That then allows you to create a wow experience for other international travellers. This is how you put brands on the map and make Brand India stronger.

We are living in an increasingly volatile world shaped by geopolitical tensions, climate events, and recurring crises. Given these uncertainties, how do hospitality groups prepare for risks they cannot fully control while continuing to invest and expand?

Safety and security is of paramount importance to all Tata Group companies. Within that, we as the hospitality arm, are more exposed to geopolitical and terror risks. We experienced the 26/11 attack on the Taj Mahal Palace, Mumbai, and remain vulnerable to events around us. We also have three hotels in Dubai, a destination that has recently been in the news because of the Iran–Israel conflict. You do what you can within your circle of control.

The second important aspect is building sustainable and inclusive tourism. Many of our destinations are somewhat overbuilt. Around 70–80% of tourism is concentrated in 10–12 locations. So, the idea is to expand, to build infrastructure and create new destinations, new beach resorts. India has a very large coastline and extensive mountain ranges. We do not just have the Himalayas; we also have the Nilgiris and the Aravallis.

In the first 75 years post-independence, growth was concentrated in certain destinations—the national capital, the commercial capital, the Golden Triangle with Rajasthan, as well as Goa and Kerala. But more new destinations and metros will emerge. Along the coast of Andhra there will be significant development. Odisha will see considerable development. In the Northeast, whatever has happened can largely be attributed to one or two brands. Much more will happen in that part of the country, enabling new destinations and helping distribute demand across a wider network of locations. That, I think, will support more sustainable tourism.

Finally, many unexplored areas will emerge, particularly those related to adventure tourism. The combination of these three factors will propel growth in a different way than we have seen in the last 20–30 years. A very important component will remain business tourism. When delegations come to India, they are likely to extend their stay by two or three days to see other parts of the country. For example, if a head of state comes to Delhi, the likelihood of also including Mumbai is high, and part of that delegation may then continue to Goa, Bengaluru, Chennai, or other destinations.

Are we mature enough to be considered a truly global hospitality market? Are we attracting large-scale international investments?

The tourism and hospitality sector is in a growth phase. It is not yet mature enough to attract large global institutional funding. Having said that, I think there is enough capital available in India. All we need is to improve the ease of doing business and reduce the number of permissions needed to build a hotel from 70+ to maybe 10+. The licences, whether a liquor licence, licence to operate, or fire licence—there are several permissions required before a hotel can be built, open, and operate.

Also, look at how we can use land that is available with clear titles, and how states can work with the Centre to develop tourism in a mission mode, identifying locations meant specifically for hotels, so that they are not priced at normal fair market value; that would help. These are the zones and hubs states will need to develop. The Honourable Finance Minister outlined in last year’s Budget speech about 50 new destinations to be developed in mission mode. I think that is good work in progress, but it needs to be expedited and pushed.

If there is one thing that the government should do in terms of policy to support the hospitality and travel industries, what would it be?

There is no one magic lever that can make tourism and hospitality part of the core strategy. However, reflecting on the last five to eight years of engaging with government officials and industry professionals, and looking at the challenges we have collectively faced. This is a sector that is evolving rapidly and can contribute strongly to Brand India.

Do you think the world truly understands India as a destination yet, or are we not telling the story right?

I would not agree to the statement that we are not telling the story right. We are not saying enough. Our international marketing budgets are quasi-non-existent. So, whatever story is being told has largely been through individual initiatives, at least in the recent past. We have been requesting the government to come up with a new version of the Incredible India campaign. That would do good for the nation. We are all working on it collectively with the Ministry of Tourism, and we hope to see some progress towards the end of this year.

Are valuations for the sector realistic, or is there a risk that the market is getting ahead of fundamentals?

Markets, in the opinion of many financial experts, are efficient. There is something called the efficient market hypothesis. When things are too low, they tend to rise, and when they go too high, they tend to correct and settle at the right level. My sole caution to hospitality investors—and also to journalists like yourself—is not to compare the PE ratios of hospitality companies in India with those in the rest of the world. Much of the world, especially in the Western Hemisphere, is largely dependent on a capital-light model. In India, we have a unique sweet spot between capital-heavy and capital-light approaches, so that in good times you benefit from operating leverage derived from capital-heavy assets, while also achieving margin expansion through the capital-light model.

Let's deal with the technology question that everyone talks about. As a hotelier, how do you approach it? Is technology really that important in running great hotels, or is the emotional connection with guests far more important?

A combination of both is needed; there is a need for technology and hospitality companies to work together. Technology is not just customer-centric. I will give you an example of artificial intelligence. With 600+ contracts in our system, we needed summaries that are easy to access, rather than reading hundreds of individual agreements just to operate hotels. AI can be used very effectively to generate structured contract summaries, with some manual fine-tuning required, as no two contracts are exactly alike.

Similarly, technology is critical for back-of-house operations, whether in ERP, cybersecurity, or many other areas where it drives efficiency and security in day-to-day business. Beyond contracts, technology also supports guest preferences, revenue platforms that enable direct bookings instead of incurring third-party costs, as well as proprietary websites and mobile apps for bookings. Loyalty programmes are another key area where technology plays an important role. Where capabilities need strengthening, companies must evaluate how best to approach it. Being part of the Tata Group, we were founding members of Tata Neu, which has helped us significantly build our loyalty customer base.

He believes that the tourism and hospitality sector is in a growth phase, and not yet mature enough to attract large global institutional funding.

Q3 FY2026 marks 15th consecutive quarter of record performance with a consolidated revenue of ₹2,900 crores, a 12% growth over the previous year, EBITDA of ₹1,134 crores and an EBITDA margin of 39.1%. The revenue in the quarter was driven by a strong same-store performance, not like-for-like growth, supported by a 17% growth in airline and institutional catering and 31% growth in New Businesses.

Puneet Chhatwal

MD & CEO, IHCL

Building an ecosystem

HCL has delivered 15 consecutive record quarters. At what point did you realise this was not just a post-pandemic rebound but a structural shift in the company’s trajectory?

The journey we embarked upon had started in early 2018 with Aspiration 2022, and we had already delivered nine consecutive record quarters till COVID struck. Those were the six quarters we lost, and the 15 that followed were again record quarters. I remain fairly optimistic that, no matter what happens, we will continue to navigate every storm, every difficulty, and keep delivering on the promise and guidance we have provided.

You have also crossed the ₹1 lakh crore market cap milestone. What does that moment mean for you as a company, and for the sector?

This is an unimaginable story because eight years ago, we were at a little under ₹13,000 crore market cap. We went much above ₹1 lakh crore, and then came down a little in the current crisis between Iran and Israel, as all stocks and capital markets are under pressure. But if you take an average over the last 12 months at around ₹1 lakh crore, it is a significant milestone. It defines the new positioning of hospitality sector stocks. More importantly, many companies have been listed in the last 18 months, which is unprecedented. India’s hospitality sector had not seen this before our strong run in the capital markets.

What do you think are the strategic decisions that created the most shareholder value?

I wish there was one magic recipe that makes it work. We have continuously delivered on growth of the top line, of people, of the portfolio, and of our brands. That leads to the second point: for any kind of growth to happen, you need a foundation, and in hospitality, your foundation is your brandscape. With 10+ hospitality brands, plus two other brands—our flight catering business, TajSATS, and our homestay business, amã Stays & Trails—we cover all customer touchpoints that are relevant for India’s customers today and in the foreseeable future.

The third important aspect: is that growth is not only by brand but also by geography and by contract type. With the exception of Taj, we have no intention of taking all brands global. There may be one-off exceptions in the Indian subcontinent with Vivanta or Gateway within a flying distance of two to three hours, similar to flying from Delhi to Chennai or Delhi to Bengaluru. Beyond that, our international focus remains on the Taj brand.

By geography, our focus remains pan-India. By contract type, we were among the first movers in shifting the definition of asset-light to capital-light. There are certain brands and businesses where it does not make financial sense to simply adopt the Western asset-light model. So we moved to capital-light, including revenue share operating leases, especially for the Ginger brand, enabling greater value creation. These were key financial drivers.

Alongside this, is the growth of people, ensuring we have the ability to absorb growth. We have grown talent from within, built over 80 skilling centres in India, trained and skilled over 40,000 youth in the last five years, and created a strong talent pipeline for the future—general managers, food and beverage managers, HR talent, and growth talent. All of this reflects a clear philosophy and strategy around people, because ultimately it is people who make the difference.

We have not forgotten the community. As defined by Jamsetji Tata, the founder of the Tata Group, the community is not just another stakeholder but the very purpose of the existence of our business. The core values that define Taj across all brands are T for the trust of all stakeholders, A for the awareness of our communities, and J for the joy in what we do, which ultimately reflects in our customer centricity in the form of Tajness. Tajness is also a leadership attribute, a way of life, and part of our DNA. Practising this authentically every day differentiates us from the rest of the world.

The combination of all these elements ultimately translates into financial performance and capital market performance.

Your earlier answers lead me to two questions. One is about geography—from a hotelier’s perspective, which states or destinations have been real game changers for IHCL? And what has made these markets real game changers?

The number one market for us has always been Mumbai. That is where we started, and with The Taj Mahal Palace alone in the ₹800+ crore club, marching steadily towards ₹1,000 crore revenue from a single hotel, it is obviously a very important property. It is well supported by Taj Land’s End,Taj The Trees, by the Gingers, President as IHCL SeleQtions, and management contracts such as Taj Santacruz. So Mumbai remains our number one, followed by Rajasthan as number two, Delhi as number three, and Goa as number four.

In terms of the number of properties, Rajasthan and Goa are among the most important, especially when I start counting the homestays. Who would have believed that we have more than 50 operational units in Goa across hotels and homestays?

What has truly been a game-changer for India and for hospitality is what Taj did 51 years ago in Goa by building Fort Aguada. A few years later, we followed in Kerala, in God’s Own Country, putting the state on the map. More recently, we have put Havelock in the Andamans on the map. As we speak today, we have received approval to start construction on the islands of Lakshadweep—Suheli and Kadmat, where, for our partners, we are already running a small resort on the island of Bangaram. Nation building, which has always been part of the ethos of the Tata Group, is strongly reflected by Indian Hotels, and especially the Taj brand, in building new destinations where few have gone before.

Ten years ago, we opened the first well-invested hotel with our own capital in Guwahati, a Vivanta. Recently, we received permission to acquire the land next to it so that the development can evolve into a Taj-branded property for the northeast. It would be unfair to cherry-pick single assets, but the journey began in 1903 with the Taj Mahal Palace in Mumbai. The second hotel was Rambagh Palace, followed by Taj Lake Palace in Udaipur. More recent additions, such as Taj Chia Kutir in Kurseong, Taj Guras Kutir in Gangtok, Taj Ganga Kutir in Raichak with the Ambuja Neotia Group, our hotels in Dubai, and the forthcoming Taj Hessischer Hof in Frankfurt, together create a diverse bouquet of Taj properties that make the brand very unique.

IHCL is currently net cash positive with strong cash flows. How do you intend to deploy capital over the next five years, and where?

We are close to ₹4,000 crores of cash reserves. There was a time three to four years ago, when we had ₹3,600 crores of debt. Today, neither the properties nor the corporation has debt, and we have cash reserves. We have communicated an estimated outlay of upto ₹5,000 cr towards existing properties and identified expansion projects over the next five years. We are also under construction, or have just started construction, on the Taj in Ranchi, another capital city in the state of Jharkhand, and have made a sliver investment in the upgradation of the Taj in Frankfurt. Many of these activities will continue. Putting the right amount of capital in India is the core of our strategy. Internationally, it will be very selective, but definitely not for any single asset acquisition.

Sustaining momentum after such growth is often a challenge. What internal disciplines have you built to ensure this performance is not just cyclical, but long-term?

It is interesting you ask this question. If you look at our recent acquisitions, they were not driven by simply adding dots on the map or more rooms to our portfolio; they were driven by a focus on our brands. If we take the ANK Hotels and Pride Hospitality acquisitions together, they allowed us to add 100+ Ginger hotels to our existing portfolio, taking the brand to a leadership position in the mid-market segment.

Similarly, when we entered wellness, we acquired a majority stake in Atmantan. This is where the beauty of hedging across volatility and extending cyclicality in the business comes in. Cyclicality will always exist, but what you can do is extend the cycle. Wellness demand tends to remain strong irrespective of market conditions. Likewise, the mid-market segment is far more resilient. It may not deliver the highest returns, but there will always be demand from travellers, whether for business or leisure.

The most important point is that these leadership teams are in place. We have put our capital behind talent. We have not just acquired portfolios of hotels or new brands; we have also brought in talent and given them the capital they may have been missing to grow further, supported by our ecosystem, commercial structure, governance structure, development and real estate teams, and project teams. Much of this is already in motion and in practice, shaping how business is being conducted across these acquisitions as well as in our traditional business.

The leader remains fairly optimistic that, no matter what happens, the Company will continue to navigate every storm, every difficulty, and keep delivering on the promise and guidance provided.

Eight years ago, IHCL was at a little under ₹13,000 crore market cap. We went much above ₹1 lakh crore, and then came down a little in the current crisis between Iran and Israel, as all stocks and capital markets are under pressure. But if you take an average over the last 12 months at around ₹1 lakh crore, it is a significant milestone. It defines the new positioning of hospitality sector stocks.

Puneet Chhatwal

MD & CEO, IHCL

Would you say that IHCL’s performance is driven not so much by the broader travel boom, but by the strategic repositioning you have undertaken over the last few years?

Performance is never driven by a single factor. It certainly helps to have a favourable demand-supply balance, where demand is outpacing supply. Another element is our comprehensive asset management strategy. We have renovated many of our older assets, and today they command a premium. The best example that comes to mind is Taj Mahal, New Delhi, where revenues increased significantly. The revenue share for NDMC went up by 80%. We invested around ₹300 crores in the property, and today we generate 2.5x more revenue than before.

Has this come only because of asset management?

No. It is also because demand has increased, and because the way we renovated was very clever and very thoughtful. There is an art and a science to renovation. Finally, you retain the core. We preserved the essence of House of Ming, Machan, and Emperor’s Lounge, while taking some of the newer concepts to another level, especially our private membership club, The Chambers, which has helped reshape how a private membership club functions, both within the Taj brand and in India.

You are building a broader hospitality ecosystem through both your own brands and acquisitions. How important is it for a hospitality group to create an ecosystem, rather than simply operate hotels?

There is no single recipe that works for all companies; there is no one-size-fits-all. As a 123-year- old company, we are in a mature phase. We have the means and the patronage of the Tata Group, which allows us to do things somewhat differently, and we are fortunate to have these advantages working for us. With changing needs and wants in India, and a growing base of around 300 million people moving towards 500 million, who will use hotels for business or leisure, the opportunity is immense while supply remains constrained. We entered at the right time with aggressive growth strategies, and they seem to have worked well for us.

Is there a segment that has surprised you with its growth beyond your flagship brand, Taj? And is brand amã a deliberate strategy or an experiment?

We have divided our company into two businesses—the traditional business and the new business, which is more like a startup that includes the reimagined Ginger, amã, Tree of Life, and Qmin. The traditional business is driven strongly by Taj. We also have three brands together— SeleQtions as a collection platform, The Gateway, and Vivanta. Atmantan operates separately. The Taj offering will be complemented going forward with luxury boutique offerings driven by both Claridges Collection as well as Brij.

So, there are three fundamental businesses: absolute luxury with boutique luxury; traditional upscale; and upper-upscale hotels with Gateway, Vivanta, and SeleQtions. The new businesses allow the company to keep experimenting. More specifically, on amã, it came purely by chance. There was no strategy initially to grow into the homestay business. It began with two villas in Goa, which, on one of my trips, I accidentally found being use—one as a skilling centre and the other as a piggery. I could not believe we had such villas in such beautiful locations being used that way. The idea was to renovate and sell them. While doing that, Tata Coffee asked if we could help with nine of their villas, followed by Tata Power with four more. Suddenly, we had 15–16 villas, and then COVID hit. That is when we created the brand amã.

It helped significantly during the pandemic, when people preferred homestays and villas over hotels. Today, we are proud to have more than 350 homestay properties either in operation or under development. It is still a small business and will become significant once we reach at least 1,000 homestays. But building a business with zero upfront capital is very unique.

The upcoming Taj Bandstand stands on the former Sea Rock site, a location deeply tied to Mumbai’s memory. How significant is this project for you, and how do you design a hotel that becomes part of a city’s cultural fabric in the way the Taj Mahal Palace has?

In this century, Taj Bandstand will definitely be an iconic asset for India and an icon on the other side of Mumbai; that is what Bandstand stands for. It is a phenomenal development, around 164 to 169 metres tall, depending on where you start measuring the height. We have all clearances in place, construction has commenced, and excavations are underway.

How do we plan such assets? It comes from years of experience and taking inspiration from other iconic developments, whether Marina Bay Sands in Singapore, Burj Al Arab in Dubai, or our own iconic asset, the Taj Mahal Tower at the Gateway of India. We study what we got right decades ago, what others may not have got right, and what we can learn—from architecture to connectivity through the sea link, the coastal road, ingress, egress, and design. Every element will be unique.

We invited four international designers to bid for the design of the property. Architecturally, we are done, and the interior design phase is underway. We will keep communicating progress over the next four to five years, as that is the kind of time required. The location requires building a significant portion of the structure in water, which means going very deep for the foundations. For such a tall structure, just the foundation itself will take a couple of years. We therefore have the time needed to design it well and create something that India will be proud of, and that can be showcased to the world.

The last two years have seen an unprecedented pricing cycle in the hotel sector. Has ADR growth peaked, or does the industry still have room to move further up the value chain?

I would like to believe there is room for further growth. For many years, from 2009 to 2019, ADR in India was flat or even below inflation levels. What we are seeing now, even after adjusting for real inflation from 2009 to 2026, suggests that we are either in line with, or still marginally below, where we should be. There is a difference between real and nominal inflation, and if you consider what was relevant between 2009 and 2012 and aggregate those figures, we remain partially or marginally below the expected level. With the anticipated increase in inflation due to rising oil and other input costs, I believe rates should continue to keep pace with other commodities.

Regarding ADR, he likes to believe there is room for further growth.

With more than 100 million members on the Tata Neu platform, you are effectively sitting on a significant opportunity. How do you plan to leverage this?

Tata Neu has more than 100 million loyalty members, and within that, the share of Indian Hotels has exceeded 15 million active users across four different categories. This has been an absolute game-changer for us. As a hospitality ecosystem, we would not have had the digital capability, the investment, or the know-how required to build such a platform independently. We are very pleased that we were founding members of Tata Neu and among the first to join the platform, and we are satisfied with the progress we have made.

Before Tata Neu, it took us 15 years to reach 2 million members. In less than four years since the launch of Tata Neu, we have grown more than sevenfold to nearly 15 million. I believe that within the next 15 to 22 months, we could cross 25 million members, making it one of the largest loyalty platforms in any hospitality ecosystem in the subcontinent.

For hotel groups with established brands that already attract strong guest loyalty, how does a programme like this add further value?

It is very interesting because we are not just building a loyalty programme. Tata Neu is a platform that also includes other Tata Group businesses. This gives us the opportunity to access customers from brands such as Tanishq or Croma, where customers are purchasing jewellery or electronics. The initial earning of points may happen more through hotels, while redemption may occur elsewhere, perhaps for an iPad or an iPhone. That may appear to be a short-term view, but over the long term the customer base expands, and eventually customers return to redeem points within the hotel ecosystem as well. It is beneficial to partner, whether with group companies or external partners. It brings group companies closer together, as marketing teams begin to collaborate, creating additional business opportunities.

In terms of loyalty behaviour, at the luxury end, loyalty is relatively less important. We are sitting here in Umaid Bhawan Palace, and it is rare for guests to come here specifically to redeem loyalty points or purely to earn them. A palace experience is not typically driven by loyalty programmes; almost 90% of guests are non-loyalty members. The programme serves more as an enabler for a small segment of customers who may not otherwise choose to spend at that level, but can experience a palace stay through accumulated points. That is the exception rather than the rule. However, loyalty becomes very important in segments such as Ginger, Gateway, and Vivanta, where customer stickiness is highly relevant. In these segments, loyalty programmes play a significant role, and we are proud to be competitive while offering strong value propositions.

Beyond numbers, how do you ensure a legacy brand such as Taj remains relevant without diluting its soul?

Brands go through different phases of their life cycle and need to evolve constantly. But when it comes to our flagship brand, I always say Taj is an emotion, and you do not play with that emotion. You keep the core and stimulate progress, and that is what we have been doing with the brand. Eight years ago, Taj had 33 hotels in operation. Today, it has 96 in operation and 46 in the pipeline. The evolution is in scale and in global recognition. Brand Finance has rated it the World’s Strongest Hotel Brand for four of the last five years; once it was ranked number two. It has also been India’s Strongest Brand across sectors for five consecutive years.

Progressing the brand every day is both an art and a science. It is an art because you cannot be too overt; you do it through a compelling proposition, walking the talk, and delivering on the brand promise. It is a science because many things must happen to remain relevant. You may not remain relevant if you are not present in resort destinations, creating new destinations, or defining new styles of service. What you did five or 10 years ago will inevitably be replicated by others. What remains truly unique is the palace proposition, the living legacies of the Taj. No one else in the world has that. We have a strong opportunity to take this palace service proposition to the rest of the world, while remaining mindful of returns. We describe it as moving from roses to ROCE— from the rose petal welcome in our palaces to return on capital employed.

Are you planning on adding any more palace properties to your portfolio?

We have been consistently adding to the portfolio. We added a palace within the grounds of a palace—Sawai Man Mahal at Rambagh Palace. We added Gorbandh Palace in Jaisalmer with Shri Ji Huzoor Maharaj Lakshyaraj Ji, and Fateh Prakash in Udaipur. We have also completely renovated Usha Kiran Palace. We are constantly evaluating palace opportunities, and one of the recent signings—the first palace in the northeast—will be Pushpabanta Palace in Agartala. Growth in this segment will not be at the pace of 10 palaces a year; it may be one palace every two years or so. But because this is our USP, something no one else in the world has, we want to maintain that position, strengthen it, and take it to the next level, including internationally.

Transforming a company like IHCL often requires decisions that may affect people or legacy structures. Were there any difficult decisions you had to make?

None of my decisions was without consensus or would be perceived as tough. We approached the transformation journey of IHCL in a way not described in any textbook. We retained all our people, believing the existing talent was outstanding and capable of delivering on the new strategy. That was perhaps the toughest positive decision we took, and it helped us significantly.

Second, we did not begin by changing Taj. We first focused on TajSATS and Ginger, as at that point, not many people paid attention to those businesses. Today, TajSATS is our second most important pillar, and Ginger is about to become the third. TajSATS crossed ₹1,000 crore in revenue last year and is growing at around 20% per annum, and Ginger is expected to reach ₹1,000 crore in the next 12 to 14 months. This was somewhat unconventional, as many would have expected changes to begin with the flagship Taj properties for quicker impact. At the time, Ginger was even seen as a challenging business, and prior to my joining, there had been discussions around possibly exiting it.

The third challenging decision related to brand structure. Before I joined IHCL, there had been a move towards a mono-brand strategy. I believed we needed to reverse that and return to a multi-brand approach, as the company had done earlier with Vivanta, Gateway, and Ginger. Given India’s heterogeneous market, this felt like the logical direction. Reversing a previously approved strategy is never easy and I must acknowledge the board’s unanimous support, which is why we stand where we do today.

Your turnaround has become a Harvard Business School case study. When future researchers study IHCL’s transformation, what decision do you hope they identify as the inflexion point?

There is no single decision because transformation is a journey. A journey is not defined by one point; it is a continuous path with many points along the way, and the culmination of those points leads to transformation. It is not like a 100m. race, a 200m. race, or even a marathon, where once you cross the finish line, the goal is achieved. Even today, we are still in the middle of the journey. We continue to evolve, reimagine ourselves, restructure the portfolio, and re-engineer our margins. There is no fixed startpoint and no fixed end point. Transformation is continuous, evolution is progressive, and the endgame depends on many factors, some of which may lie beyond our circle of control. What remains within our circle of influence and control, we navigate to the best of our ability.

Eight years ago, IHCL was at a little under ₹13,000 crore market cap. We went much above ₹1 lakh crore, and then came down a little in the current crisis between Iran and Israel, as all stocks and capital markets are under pressure. But if you take an average over the last 12 months at around ₹1 lakh crore, it is a significant milestone. It defines the new positioning of hospitality sector stocks.

A journey is not defined by one point; it is a continuous path with many points along the way, and the culmination of those points leads to transformation.

I see hospitality and tourism contributing at least 10% to India’s GDP and over 10% of jobs. This is not a far-fetched number. Rajasthan already contributes around 17%, and Goa is also north of 17% in terms of GDP contribution. There are many destinations in India that have not yet even started running, forget reaching their potential.

Puneet Chhatwal

MD & CEO, IHCL

Legacy and the human core of hospitality

You have provided international exposure opportunities to many of your colleagues. What was the thinking behind this, and how has it benefited the group?

Any kind of exposure is fundamental to gaining knowledge. And as I am a product of the East and the West, I do believe that the journey to the western part of the world did shape me in the way I am today. So why limit it to myself? When I returned to India, I thought of sharing the platform reforms that I was privileged to experience with all colleagues in the company. And one thing led to the other.

So from the topmost management to junior-most management, we created a lot of programs, not just offering certification but also real-life experience—from advanced management programs for the top leadership of the company at Ivy League, INSEAD, Harvard, Stanford, etc., to Executive MBA programs with La Roche-Glion, ESSEC, Bocconi, including with TMTC, that’s the Tata Training Center, as well as exchange programs with our hotels in Dubai, so that people could go to Dubai and experience our wonderful cuisines there, and for people in Dubai to come and experience Indian cuisines in India.

You once said success in hospitality requires a clear strategy backed by action, not optimism alone. How has that philosophy guided you as a leader?

As I mentioned on one of the other platforms, strategy talks, but execution walks. It's very important to execute on the plans that you have had, unless circumstances force you to freeze execution, which happens once in 30, 40, 50 years, like in a pandemic or a war situation. I have personally believed you go in for execution. What does not work, you correct later. But the important thing is to start, and there is no right time to start. The best time to start is now, and that has worked very well in my life. I have tried to inculcate that idea in my colleagues, in the people I work with, and I work for.

How do you balance culture, instinct, and data when leading a global hospitality organisation?

I always say in lighter moments that culture eats strategy—not just for breakfast, but for breakfast, lunch, high tea, and dinner. Culture is really the bedrock of any kind of business, and within hospitality, culture plays a very important role because you're being a host, and at the same time, you have to use

all the business tools provided to you. So I think one thing does not exclude the other. Customer centricity driven by good culture and some kind of science of business parameters is an unbeatable combination, and I would encourage everyone to practice those with their heart and soul.

And what has travel itself taught you about people and cultures that leadership textbooks never could?

There's something about travel—some words which I think describe travel, whether you call it teachings or you call it experience. But for me, number one is exposure, number two is tolerance, and number three is resilience. So ETR—E for exposure or experience you gain while travelling; T for tolerance for various cultures, various situations, and for all that happens around you and how you go about dealing with it; and R for resilience. I think nothing builds a better resilience model than travel, and that has been aptly demonstrated during and post-COVID. If there is one sector that was once declared gone forever yet could bounce back with great elan, it is tourism and hospitality.

How has your leadership style evolved over the years?

The professional keeps evolving, and every chapter of your journey is important and different. When you start as a management trainee or in some form of management training, the needs are very different. When you become a young manager, when you become an international manager, and then when you head a company, it is all very different. So I have not done anything differently today. But when you are leading an organisation of 45,000+ people, you cannot act as a young manager or a young trainee. I think each chapter is important. Each person who mentored you, who guided you, is an important part of that chapter. And ultimately, you reach a point where you have to lead, and you cannot take as many risks as you might have taken in your 20s and 30s.

If a young hotelier asked you to name one thing about the industry that nobody tells you when you start, what would your answer be?

I would say this is a sector in which you have to lead with compassion, and everything else is business of common sense, hard work, dedication and focus. But never forget the compassion. Be it for guests, for your customers, for your employees, associates, stakeholders, suppliers, and the entire ecosystem of stakeholders that you're dealing with.

You've spoken about hospitality as a business built on relationship capital. What does that mean in practice for hotel leaders like you?

I think relationship capital is fundamental to succeeding in any business, especially those directly related to customers. If you cannot build a relationship or that bond with your customers, with the people you work with, then this is not the business for you. You need to be able to build bridges with all the people you work with and you work for, including the ones you serve. And whenever you serve, serve with care, because that builds the bridge or the relationship. Compassion and caring have no substitutes in the world of hospitality.

“I always say in lighter moments that culture eats strategy—not just for breakfast, but for breakfast, lunch, high tea, and dinner,” says the CEO.